The Cyprus Intellectual Property (IP) regime provides for an 80% exemption on qualifying profits derived from the use of qualifying intangible assets, resulting in an effective taxation of only 20% of such income. In practical terms, this may reduce the effective tax rate to as low as 3% on eligible IP-related profits.

Cyprus has implemented Action 5 of the OECD Base Erosion and Profit Shifting (BEPS) initiative, which introduces the “modified nexus approach”. This requires a direct link between the income generated from intellectual property rights and the qualifying expenditure and activities undertaken by the taxpayer contributing to that income.

Qualifying assets under the Cyprus IP Box Regime

“Qualifying intangible asset” means an asset that was acquired, developed or used by a person for the carrying on of the business and that constitutes intellectual property excluding intellectual property that relates to marketing and that is the result of activities of research and development and includes intangible asset for which there is only economic ownership.

Qualifying intangible assets include:

- Patents as these are defined in accordance with the provision of the Patent Law,

- Computer software programs;

- Other intangible assets which are legally protected and fall under the provisions of (a) or (b) below:

- utility models, intellectual property assets which provide protection to plants and genetic material, orphan drug designations and extensions of protections of patents

- that are non-obvious, useful, and novel, where the person which utilizes them for the carrying on of the business does not generate annual gross income exceeding Euro 7.500.000 per annum from all intangible assets and in the case of a group of such persons, the group does not generate annual gross income exceeding Euro 50.000.000 on a worldwide basis, using an average of 5 years for both calculations of the aforementioned amounts, but they are not tradenames (including brands), trademarks, image rights and other intellectual property rights used to market products and services.

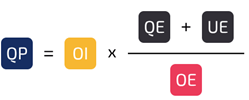

The Nexus Approach

The Nexus Approach is used to determine the amount of qualifying profits that will give the relevant deduction to the taxpayer.

Qualifying profit (QP) is defined as the proportion of the overall income (OI) derived from the qualifying asset, corresponding to the fraction of the qualifying expenditure (QE) plus the uplift expenditure (UE) over the overall expenditure (OE) incurred for the qualifying intangible asset.

Overall Income (OI)

Overall income is defined as the gross income earned from qualifying intangible assets during the tax year, minus any direct costs incurred for generating the income.

On calculating overall income, direct costs include as follows:

- All direct or indirect costs incurred in earning the income from the qualifying asset

- The amortization of the cost of the assets

- Notional interest in equity contributed to finance the development of the asset

Qualifying Expenditure (QE)

Qualifying expenditure for a qualifying intangible asset is the sum of all research and development (R&D) expenditure that took place during any tax year wholly and exclusively for the development, improvement or creation of the qualifying intangible asset and that relate directly to the qualifying intangible asset.

Qualifying expenditure includes, but is not limited to, the following:

- wages and salaries

- direct costs

- general expenses relating to installations used for research and development;

- expenses for commissions related to R&D activities

- expenses associated with R&D that have been outsourced to non-related persons

Uplift Expenditure (UE)

An uplift expenditure, which will be equal to the lower of:

- 30% of the qualifying expenditure

- Total cost of acquisition of the qualifying intangible assets, plus the cost of outsourcing to related parties of any R&D activities in relation to such assets

Overall Expenditure

Overall expenditure relating to qualified intangible assets is defined as the sum of:

- Qualifying expenditure and

- Total amount of acquisition cost and cost of outsourcing of research and development activities to related parties, in relation to qualifying intangible asset, that was incurred in any tax year.

How can we help

At FINCAP Advisers Ltd, our dedicated tax team offers comprehensive services, including:

- Corporate and international tax advisory

- Personal tax planning and compliance

We combine technical expertise with practical solutions to help clients navigate the evolving tax landscape efficiently and confidently.

Should you like to further discuss the content and potential impact of the above to your business, please contact our trusted advisors from the Tax Department.